Week ahead

With the fourth quarter of 2019 finally underway, markets await third-quarter (Q3) gross domestic product (GDP) readings to assess the resilience of the global economy, which significantly slowed in the second quarter.

The first major country to report GDP is China, which is expected to slow further amid ongoing trade tensions. Although China-US trade negotiations restarted at the beginning of the month, little progress has been made, with both countries entrenched in their positions.

While Chinese Q3 growth has likely been supported by a more dovish monetary policy, after the People’s Bank of China lowered banks’ reserve rate over the summer, further easing is unlikely. We believe that a boost in fiscal policy and a truce with the US, in particular, should be the most effective tools to sustain the economy.

In the US, the negatives of rising protectionism and a global slowdown have so far been contained to the manufacturing sector and mitigated by the US Federal Reserve’s more dovish stance. However, with weakness in manufacturing now spreading to services, it will take more than accommodative policies to ease investors’ concerns. Markets will welcome any signs of stabilisation in September’s industrial production and a pick-up in October’s Federal Reserve Bank of Philadelphia business index following last month’s disappointing print. That said, a sustained rebound in business activity will be contingent upon progress on the trade front.

The eurozone’s harmonised index of consumer prices and UK’s consumer prices index are both due out next week and are likely to be on the soft side in September, providing a tailwind to consumers. A combination of low inflation and steady wage growth has helped boost consumer purchasing power over the year. Household spending has effectively kept afloat European economies in 2019 in the face of Brexit woes and external demand shocks. However, while the Brexit saga unfolds, investors should keep an eye on sterling as sharp currency depreciations could lead to a significant pick-up in UK inflation.

Chart of the week

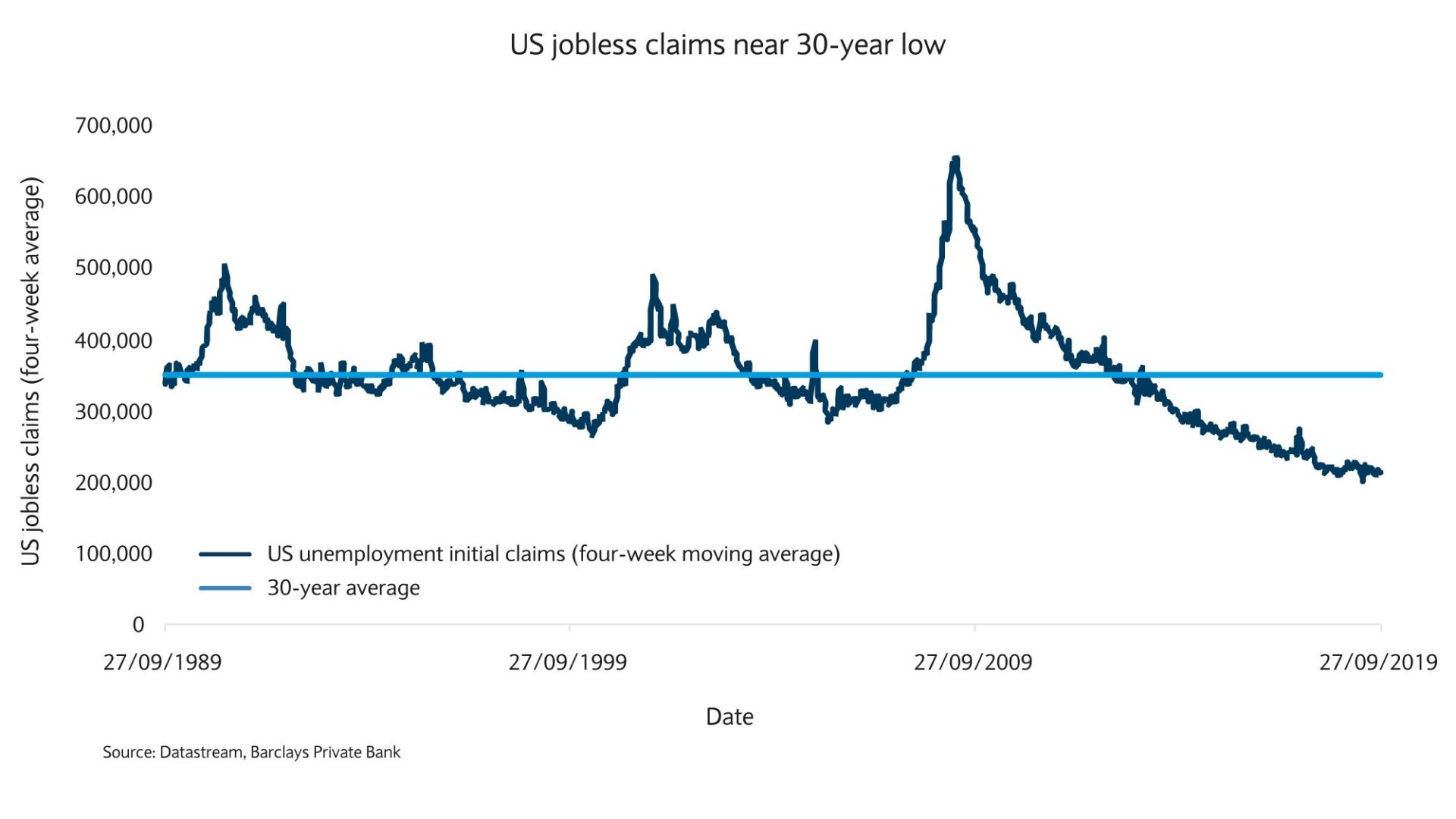

Recession fears misplaced, for now

While global manufacturing is contracting and services activity has been slowing, consumers’ health has been resilient so far. Monitoring consumer spending is critical in assessing whether a recession is brewing, given that consumption is the single largest contributor to most economies’ growth.

Unfortunately, the labour market tends to be a lagging indicator and so its predictive abilities are limited. Yet, we believe it can help confirm or counter signals sent by other indicators.

In particular, the weekly jobless claims statistics are helpful in tracking tipping points in the labour market. And here, signs are rather encouraging. Indeed, the series’ four-week moving average remains well below its long-term average.

In fact, according to US Federal Reserve economist Claudia Sahm, a prolonged and significant deterioration in the labour market is needed before a recession becomes a real possibility. Indeed, according to Sahm’s work, which has predicted every recession since 1970, the three-month average unemployment rate needs to climb by 0.5 percentage points from its lowest level over a period of 12 months for gross domestic product to contract for more than two consecutive quarters.

To put this into context, the US economy has to generate around 100,000 jobs per month to keep the unemployment rate unchanged, assuming the participation rate remains stable. With the rate sitting at an historical low of 3.5%, the Sahm rule requires unemployment to jump to 4% within the next year to ring a recession alarm. This translates into an average of only 25,000 jobs created per month (compared with the 136,000 created in September).

As such, unless the US economy starts destroying jobs in the next few months, we believe that a recession looks unlikely in the next 12 months.

A man from Nice used a stolen bank card to make purchases in Monaco, spending over €1,700 in various shops, mostly on airpods that he planned to resel...

Read More

Read More

Electric bike-sharing firm Pony says all of its vehicles will be back out on the streets of Nice no later than June, after they were withdrawn last mo...

Read More

Gabriel Attal announced new measures In response to recent acts of violence among young people during a visit to Viry-Châtillon. Attal highlighted the...

Read More

The owners of a vast floating artificial island that had been planned for last summer off the coast of Mandelieu have won a legal battle to be allowed...

Read More

The Monegasque State has successfully conducted its first national voluntary surrender operation, with 123 firearms being handed over by private indiv...

Read More