Week ahead

Next week is a heavy one for key macro data in leading regional economies, as investors remain on tenterhooks due to heightened risk-off sentiment.

In the US, August’s consumer confidence and the University of Michigan consumer sentiment surveys will hint at the outlook for domestic spending, which is expected to remain resilient despite the US slowdown. This is likely to be confirmed by the second estimate for second-quarter gross domestic product, which is also out next week. July’s core personal consumption expenditure index, the Fed’s preferred measure of inflation, is likely to stay subdued and should warrant further easing from the US central bank.

In the eurozone, markets will eye a series of surveys with economic conditions in the region worsening significantly in recent weeks. August’s business climate and economic sentiment surveys are likely to confirm a deterioration in the economic backdrop amid escalating trade tensions and domestic geopolitical issues (Brexit and threats of a general election in Italy), while August’s consumer confidence data should broadly hold up. We expect July’s unemployment rate to confirm the resilience of the eurozone’s labour market, while August’s harmonised indices of consumer prices flash readings should remain muted.

Until we have more clarity on Brexit, UK macro indicators are set to remain relatively steady. We expect July’s Bank of England consumer credit data to be on the soft side. August’s Nationwide house prices and July’s mortgage lending readings will show the strength of the housing market.

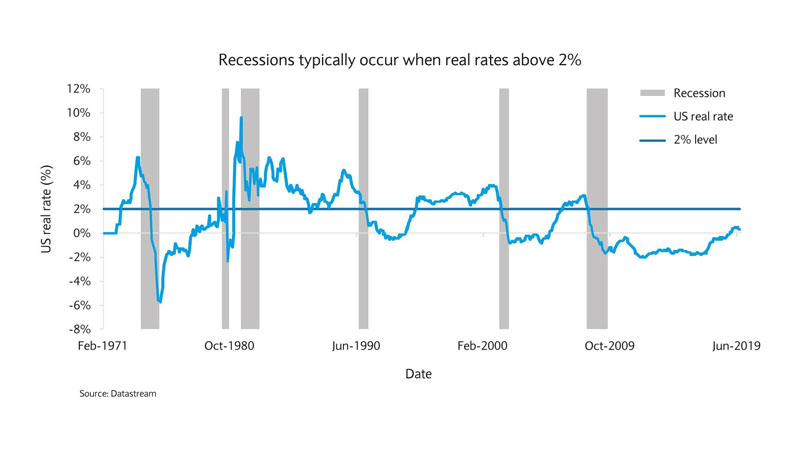

Chart of the week

Recession watch

For indications of when the next recession might strike, the real interest rate (ie adjusted for inflation) is one indicator to turn to. Economic theory suggests a statistical relationship between an economy’s real interest rate and the growth in its gross domestic product. Specifically, the real rate should approximate to the growth rate of the economy and hover around a long-term level of 2%.

A level of around 2% suggests that real rates are not too loose or too tight, and are conducive to the economy expanding at its long-term average pace.

Historically, real rates have been a reasonable indicator of the likelihood of recessions (ie at least two consecutive quarters of economic contraction), with recessionary periods corresponding to a backdrop of real rates above 2%. At those times, excesses in the economy generally led the US Federal Reserve (Fed) to raise interest rates. By contrast, an overly-tight monetary policy had the adverse effect of hindering growth and triggering a recession.

US monetary policy is currently loose and real rates are well below 2%. Although fears of a shrinking US economy have risen due to trade tensions and fading economic momentum, the next recession still seems at least twelve months away going by the historical relationship between recessions and real rates.

Moreover, given uncertainties around trade tensions and geopolitical risks (such as Brexit and potential Italian elections), companies are delaying investments and so creating a more sluggish growth environment, rather than an outright recession.

The lack of major excesses in the economy, coupled with a dovish US central bank, means that real rates are set to stay below 2% for the time being, providing some breathing space ahead of the next recession.

Gabriel Attal announced new measures In response to recent acts of violence among young people during a visit to Viry-Châtillon. Attal highlighted the...

Read More

Read More

The owners of a vast floating artificial island that had been planned for last summer off the coast of Mandelieu have won a legal battle to be allowed...

Read More

The Monegasque State has successfully conducted its first national voluntary surrender operation, with 123 firearms being handed over by private indiv...

Read More

A hospital in Cannes has had to postpone all non-urgent consultations and operations after falling victim to a cyberattack....

Read More

Potential presence of broken glass in pizzas. A recall has been issued for several pizzas distributed by Auchan Avallon in France due to the potential...

Read More