Week ahead

After a busy two weeks of quarterly corporate earnings data, this week has some key economic data points to watch out for.

On Monday the Conference Board’s January US consumer confidence index reading is out. Consensus is for an increase in the index by 0.7 percentage points to 127.2, which is understandable given the signing of the “phase one” trade deal with China.

On Tuesday the January Nationwide house price index data for the UK is published, which may reveal the extent of any initial post-election bounce in activity in the housing market.

Undoubtedly, top of investors’ calendar is the US Federal Reserve (Fed) and the Bank of England (BOE) policy meetings on Wednesday and Thursday respectively. Whilst the market believes that the Fed has accomplished its “insurance cut” mission, and will leave interest rates unchanged, predicting the outcome of the BOE meeting is tougher given weak pre-election data and lack of clarity since.

The fourth-quarter (Q4) flash estimate of US gross domestic product (GDP) is revealed on Thursday. On a seasonally-adjusted annual rate basis, consensus is for an unchanged reading from the previous quarter at 2.1%.

Finally, eurozone preliminary Q4 GDP data is announced on Friday and will show whether growth has started to recover since news on the phase one trade deal and Brexit uncertainty reduced. Subdued inflation remains a key talking point and the week ends with January’s flash eurozone harmonised index of consumer prices and December’s US core personal consumption expenditure index data. Consensus for the latter is for a 0.1pp rise to 0.2% on a month-on-month basis.

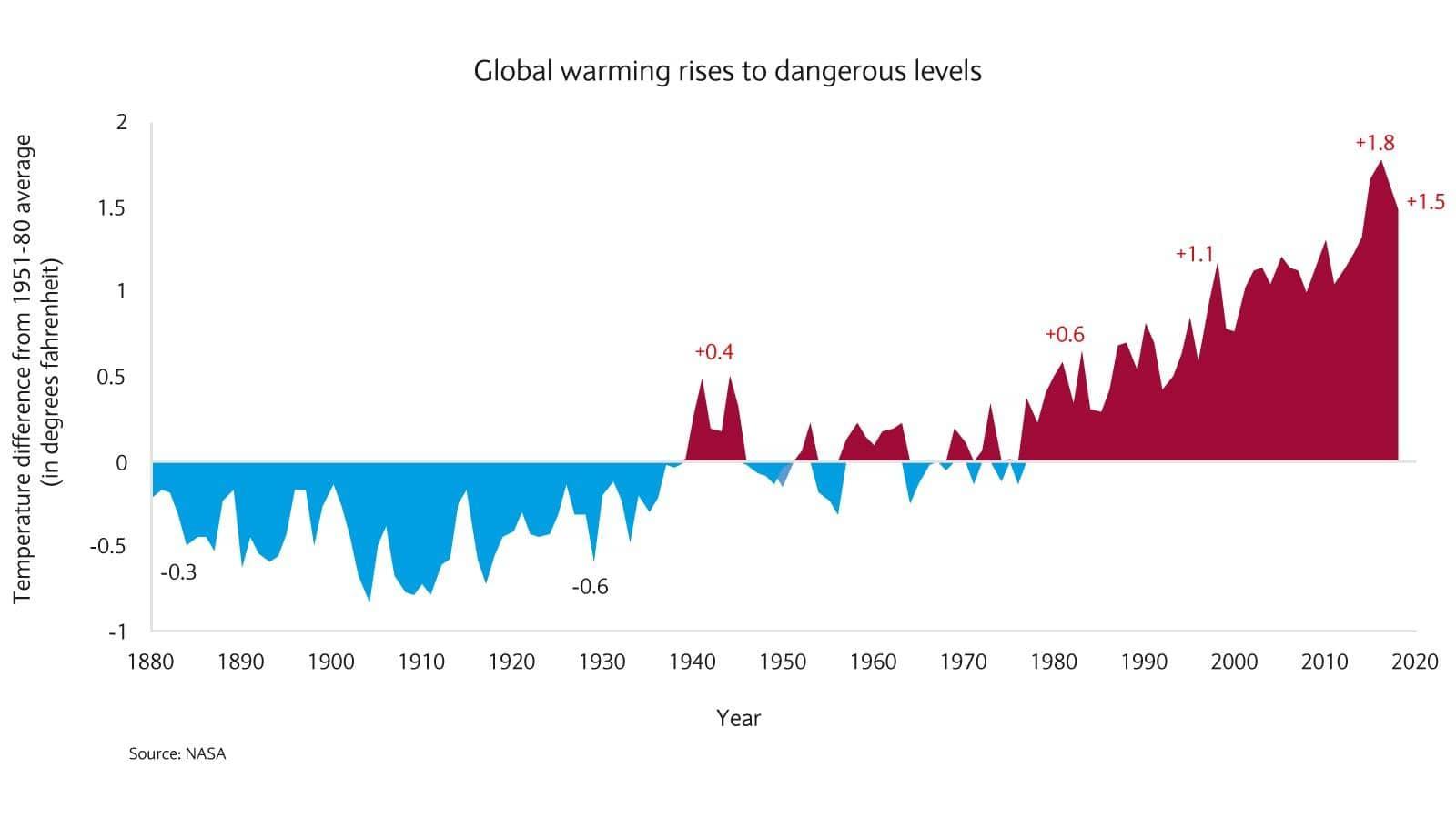

Chart of the week

Climate change: time for investors to evolve

The last decade was the warmest since records began in 1850 and projections anticipate that temperatures will get hotter still.

Climate change has become a priority for many financiers, business leaders and politicians alike. For instance, climate change is a focus topic at this month’s World Economic Forum in Davos. However, solutions to one of the world’s most pressing challenges may not be emerging fast enough.

The increase in average temperatures is the primary indicator of climate change and driver of many of its effects. Since 1850, 17 of the warmest years on record have occurred in the last 18 years. The world is on average one degree Celsius hotter than it was between 1850 and 1900 (see chart). An increase of one additional degree to average annual temperatures is seen as the threshold to “severe, widespread, and irreversible” effects of a climate breakdown.

In addition to the temperature record, ocean temperatures last year were the highest on record – leading to more ocean acidification, sea-level rise and extreme weather. Both of these measures indicate that the “climate crisis” has reached a new level and rapid measures are needed to speed up the process of cutting greenhouse gas emissions.

With climate seemingly inevitable in an uncertain world, investors can no longer disregard the risks when making investment decisions. Industries and companies working towards reducing the impact of climate change, accelerating energy transition and improving infrastructure are likely to profit the most from increased spending and accommodative policy measures focused around climate change.

Electric bike-sharing firm Pony says all of its vehicles will be back out on the streets of Nice no later than June, after they were withdrawn last mo...

Read More

Read More

Gabriel Attal announced new measures In response to recent acts of violence among young people during a visit to Viry-Châtillon. Attal highlighted the...

Read More

The owners of a vast floating artificial island that had been planned for last summer off the coast of Mandelieu have won a legal battle to be allowed...

Read More

The Monegasque State has successfully conducted its first national voluntary surrender operation, with 123 firearms being handed over by private indiv...

Read More

A hospital in Cannes has had to postpone all non-urgent consultations and operations after falling victim to a cyberattack....

Read More