Week ahead

The week ahead hosts the moment markets have been desperately waiting for - the July Federal Reserve meeting on Wednesday.

Investors are divided on whether we will see a 25 basis point (bps) or 50bps cut in interest rates. So the outcome will have significant implications for bond and equity markets, as well as global central bank policy.

While the Fed meeting is likely to draw most of the attention, there is also the Bank of England meeting on Thursday.

In the UK, June money and credit data will be released on Monday. Growth in unsecured credit has lagged recently but housing market activity has held up, stemming from low mortgage rates and real earnings growth. IHS Markit’s July manufacturing purchasing managers’ index (PMI) follows on Thursday and construction data on Friday. Brexit uncertainty is likely to continue to negatively skew these two surveys, both below 50 and indicating contraction, with construction falling in June to its weakest level since April 2009.

Expectations

In the eurozone, Tuesday sees a variety of July confidence and sentiment indicators. Wednesday is due to see the preliminary data for second-quarter gross domestic product, with the consensus expecting growth of 0.2% quarter on quarter, July’s flash harmonised index of consumer prices reading and the unemployment rate. The July final reading of the manufacturing PMI is on Thursday, with Friday closing the week with June’s producer prices index and retail sales data.

Moving back across the Atlantic, the June personal consumption expenditure data is on Tuesday, with May’s core year-on-year deflator reading 0.4 percentage points below the 2.0% Fed target. Other key data on the health of the economy include the closely watched Institute for Supply Management’s manufacturing index reading for July on Thursday and the July unemployment and non-farm payroll numbers on Friday.

A quiet week in China sees the July official non-manufacturing, manufacturing and services PMI numbers on Wednesday.

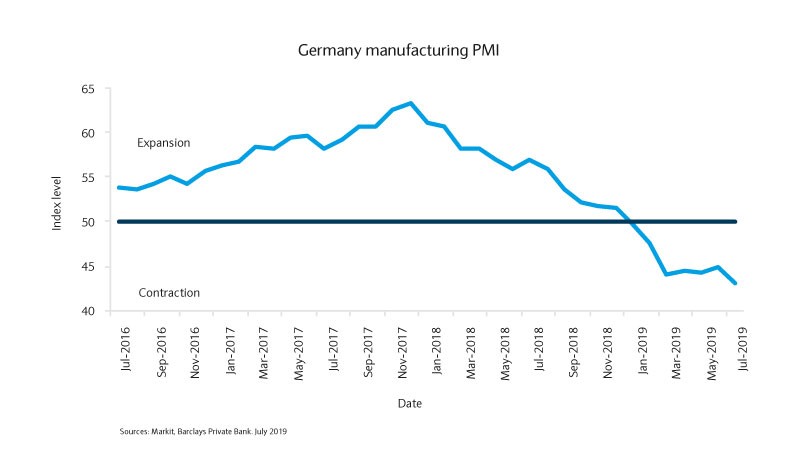

Chart of the week

Manufacturing stutters

At first glance the manufacturing data for July look challenging, particularly in the eurozone. The initial estimate of the HIS Markit purchasing managers’ index (PMI) show that manufacturing activity in the region contracted for the sixth consecutive month. The biggest surprise came from Germany where the index fell to 43.1, a 7-year low, well below the 50 level that separates expansion from contraction. While services companies have so far fared better, it is clear that manufacturing is on the verge of entering a recession, led by auto manufacturers.

It’s difficult to gauge how much of this slowdown is directly linked to trade tensions, but with limited progress being made on this front few expect a quick turnaround. Yet, we believe that, in Germany and globally, we may have reached the trough and that thanks to a combination of upcoming monetary and fiscal stimulus, economic activity should stabilise gradually in the second half of 2019.

The Côte d'Azur is on alert for a surge in imported cases of dengue fever. Since the beginning of 2024, a record 1,679 imported cases have been record...

Read More

Read More

The post-mortem will take place next Monday for a 33-year-old man whose body was recently found in the Var after being missing for more than a month....

Read More

French scientists have been developing technological tools for the past four years to help athletes optimize their training for the Paris 2024 Olympic...

Read More

Nice airport says as many as 60% of flights will be cancelled tomorrow due to a nationwide strike by air traffic controllers....

Read More

After eight months of work and several sea trials, the French aircraft carrier Charles de Gaulle has begun a six-week operation in the Mediterranean, ...

Read More