Week ahead

Survey data on the health of leading economies kicks off the week, with the final January purchasing managers’ index (PMI) readings from China, the eurozone, the UK and the US.

China’s Caixin and the US IHS Markit PMI data have both indicated that the two economies have managed to keep expanding. With the recent improvement in trade talks, the final data will reveal if growth can be furthered. With regards to the US, the Institute for Supply Management readings will be closely watched after they signalled contraction in manufacturing in recent months.

The PMI data will reinforce whether the UK has experienced a post-election bounce in manufacturing and services activity, as the flash PMI indicated, and if the eurozone continues to show signs of recovery (albeit from a contracting manufacturing base) in the midst of easing global trade tensions.

In the eurozone, the consumer has managed to keep the economy afloat. December retail sales data on the Wednesday will show if consumption strengthened in the run-up to Christmas, after 2.2% year-on-year growth in November.

Ending the week is the January non-farm payrolls data in the US. While the unemployment rate remained at noticeably low levels in December at 3.5% and real earnings remain positive, the non-farm payroll number disappointed in December at 145,000, especially given the revising lower of employment readings in prior months.

January trade data from China is also on Friday. The data will reveal the impact on the country’s export-heavy economy of a recent de-escalation in trade wars with the US and the signing of the “phase-one” deal. December’s trade surplus was revised up $0.5bn to $47.2 bn.

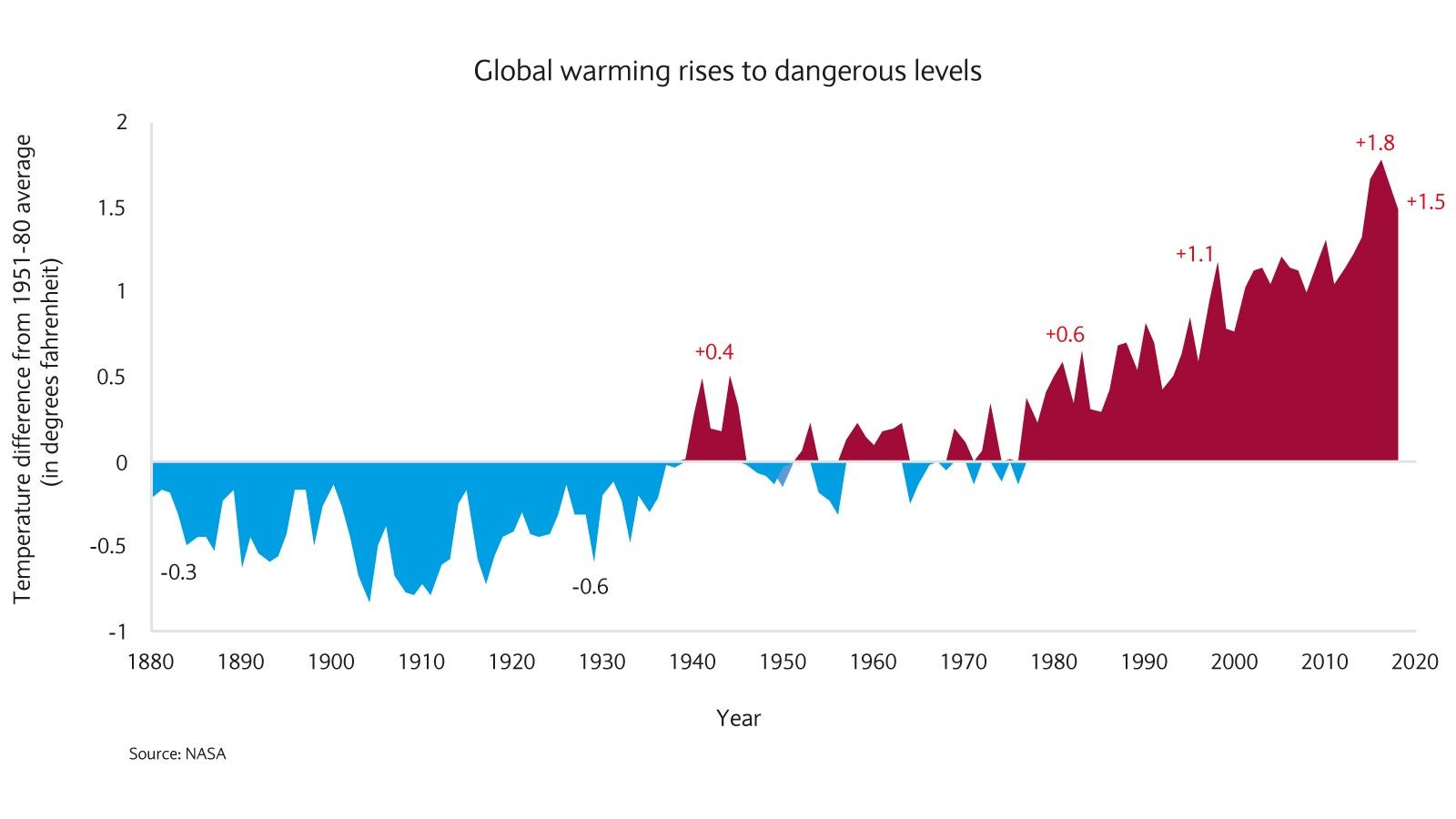

Chart of the week

Climate change: time for investors to evolve

The last decade was the warmest since records began in 1850 and projections anticipate that temperatures will get hotter still.

Climate change has become a priority for many financiers, business leaders and politicians alike. For instance, climate change is a focus topic at this month’s World Economic Forum in Davos. However, solutions to one of the world’s most pressing challenges may not be emerging fast enough.

The increase in average temperatures is the primary indicator of climate change and driver of many of its effects. Since 1850, 17 of the warmest years on record have occurred in the last 18 years. The world is on average one degree Celsius hotter than it was between 1850 and 1900 (see chart). An increase of one additional degree to average annual temperatures is seen as the threshold to “severe, widespread, and irreversible” effects of a climate breakdown.

In addition to the temperature record, ocean temperatures last year were the highest on record – leading to more ocean acidification, sea-level rise and extreme weather. Both of these measures indicate that the “climate crisis” has reached a new level and rapid measures are needed to speed up the process of cutting greenhouse gas emissions.

With climate seemingly inevitable in an uncertain world, investors can no longer disregard the risks when making investment decisions. Industries and companies working towards reducing the impact of climate change, accelerating energy transition and improving infrastructure are likely to profit the most from increased spending and accommodative policy measures focused around climate change.

After eight months of work and several sea trials, the French aircraft carrier Charles de Gaulle has begun a six-week operation in the Mediterranean, ...

Read More

Read More

A group of experts have come up with more than 150 recommendations for how Nice can deal with the increasing effects of climate change....

Read More

Some communes in the Alpes-Maritimes will be plunged into darkness this Monday evening. For the third year running to mark Earth Day, mayors in the Al...

Read More

Gendarmes in the Var have appealed for information after a 34-year-old man went missing in Cavalaire-sur-Mer....

Read More

A man from Nice used a stolen bank card to make purchases in Monaco, spending over €1,700 in various shops, mostly on airpods that he planned to resel...

Read More