Week ahead

Late June is heating up as markets approach next week’s long-awaited G20 meeting of world leaders and a series of end-of-month indicators.

Investors will hope for some signs of easing US-China trade tensions as talks between presidents Trump and Xi are likely to resume at the G20 meeting. This is the main event concerning China over next week while the economic calendar in the region remains relatively quiet. The US has a busier schedule, with personal consumption expenditure (PCE) readings for May coming out and inflation expected to remain muted as trade tensions fail to exert significant upward pressure to prices.

Major surprises are unlikely in the final data for first-quarter gross domestic product and PCE, while June’s University of Michigan Consumer Sentiment Index and May’s overall PCE will give a clearer picture of the current state of the economy.

In the eurozone, we expect a similar pattern of data. In line with the US, May’s consumer price index and June’s flash harmonised index of consumer prices should continue to be on the soft side despite consumer spending remaining resilient. June’s consumer confidence readings for both the eurozone and the UK will indicate what shape the two region’s economies are in one month after the European parliamentary elections took place. June’s Nationwide House Prices and May’s Finance Mortgage Approvals will help investors assess the health of the UK housing sector.

Chart of the Week

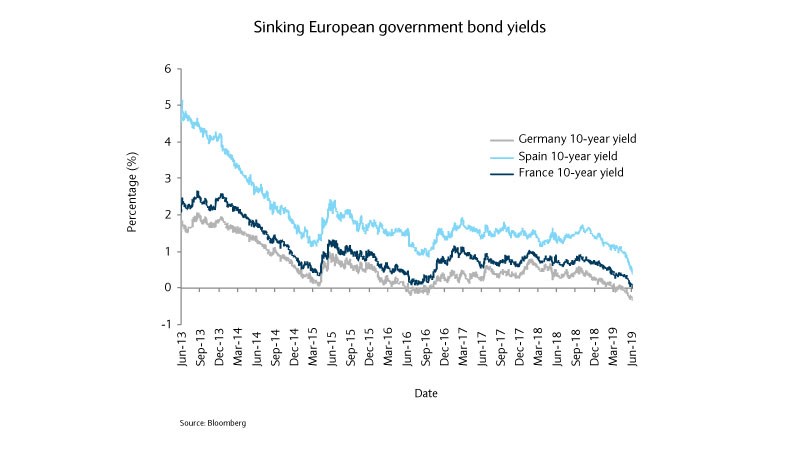

European negative yields increasingly the norm

European Central Bank (ECB) President Mario Draghi hinted this week that further stimulus could be warranted should inflation persist at depressed levels or the macro outlook further deteriorates. The ECB appeared to be preparing the markets for further rate cuts which resulted in bonds rallying across the region and yield curves declining sharply for longer maturity issues.

Negative yielding debt globally is now for the first time greater than $13tn, with $1.2tn being bought into this week. German 10-year yields fell deeper into negative territory to a record low, while French yields dropped to 0% for the first time. Yields on peripheral bonds plunged too, as Italian yields lost 18bps and Spanish 10-year yields fell to a record low of 0.40%.

The dramatic decrease in yields is likely to push institutional investors who are mandated to buy European bonds into areas that are still providing positive yields; likely found within longer dated and investment grade bonds. As a result, we would expect spread compression in investment grade bonds.

A Self-service rental system for paddle boards has been implemented on the Larvotto beach in Monaco. Users can access the equipment through a paying a...

Read More

Read More

French president Emmanuel Macron has called for stronger, more integrated European defences as he outlined his vision for a more assertive European Un...

Read More

The Côte d'Azur is on alert for a surge in imported cases of dengue fever. Since the beginning of 2024, a record 1,679 imported cases have been record...

Read More

The post-mortem will take place next Monday for a 33-year-old man whose body was recently found in the Var after being missing for more than a month....

Read More

French scientists have been developing technological tools for the past four years to help athletes optimize their training for the Paris 2024 Olympic...

Read More